SMM News on July 31:

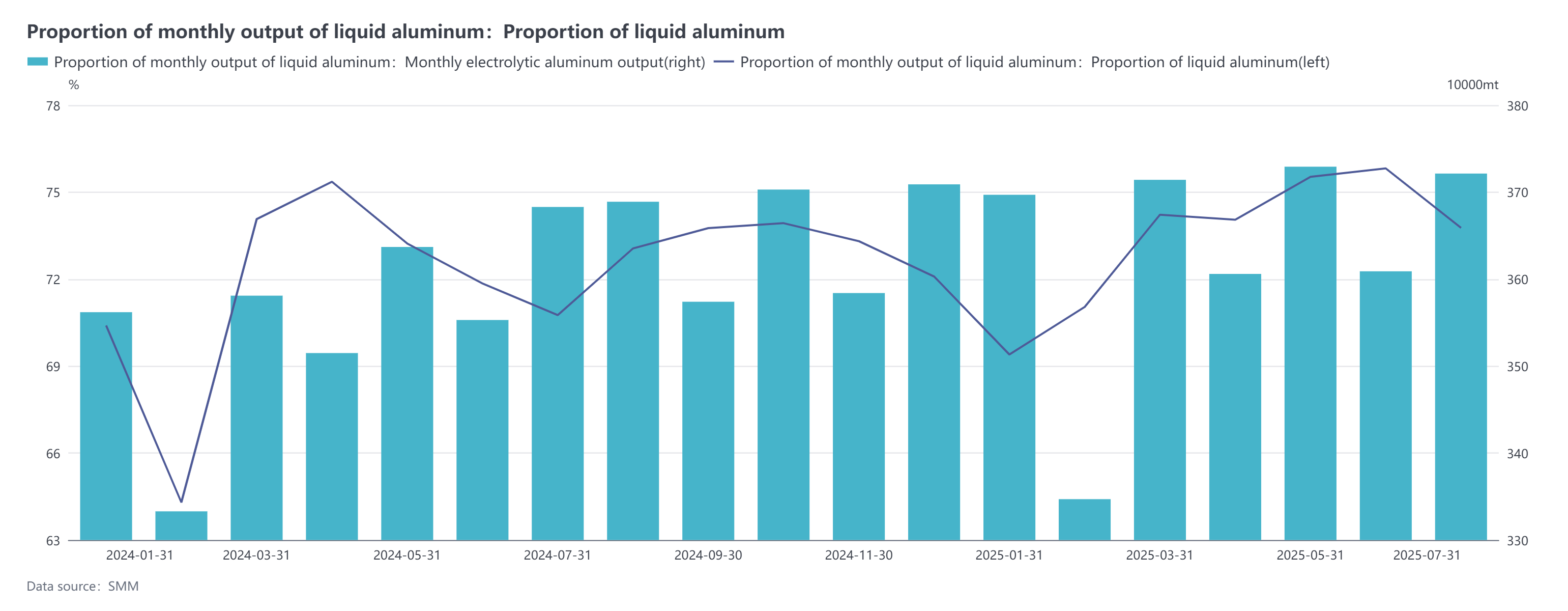

According to SMM statistics, domestic primary aluminum production in July 2025 (31 days) increased by 1.05% YoY and 3.11% MoM. The operating capacity of primary aluminum in China increased slightly MoM in July, mainly due to the start-up of the second-phase replacement project of primary aluminum in Shandong-Yunnan. With the strong off-season atmosphere in the end-use market, alloy production cuts were significant across the country. As a result, the proportion of liquid aluminum in domestic aluminum smelters declined significantly in July, with the industry's proportion of liquid aluminum falling by 2.06 percentage points MoM to 73.77%. Based on SMM's data on the proportion of liquid aluminum, the domestic casting ingot volume of primary aluminum in July decreased by 9.34% YoY and increased by 11.89% MoM to approximately 976,300 mt.

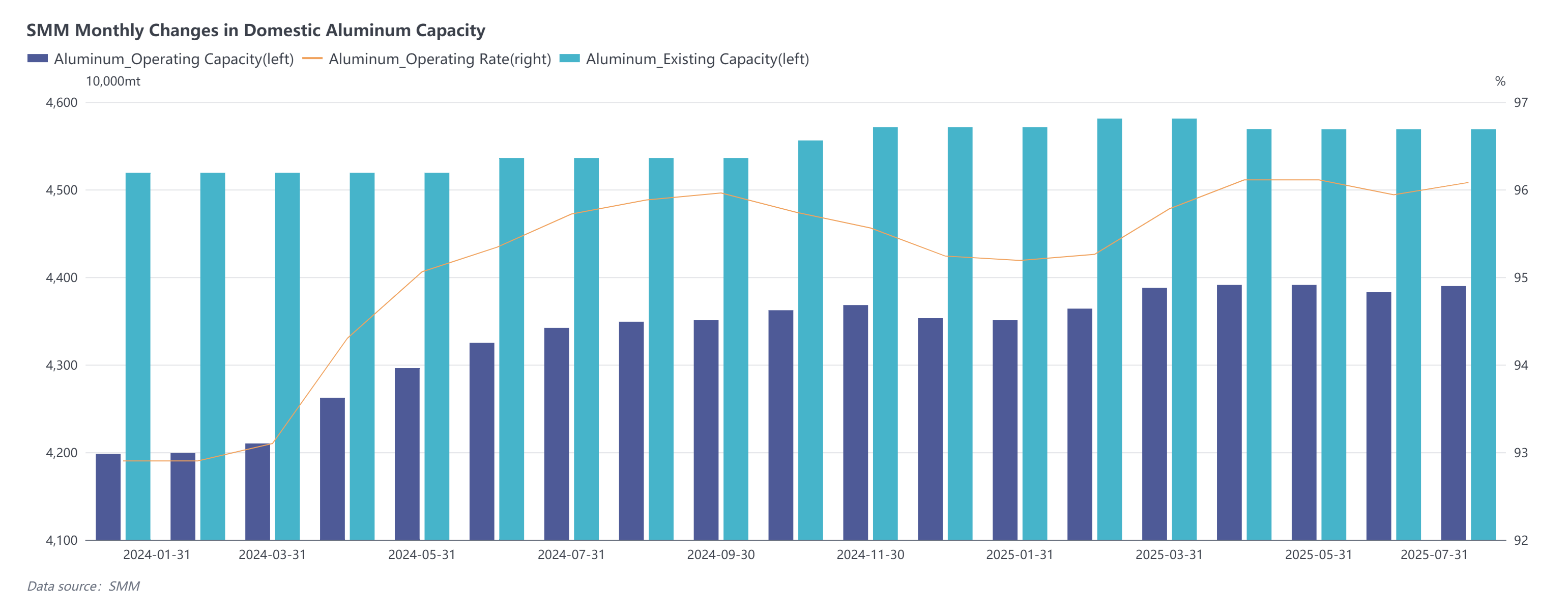

Capacity Changes: As of the end of July, SMM statistics showed that the existing capacity of primary aluminum in China was approximately 45.69 million mt (SMM made revisions in late April after considering capacity replacement and the demolition of old plants, eliminating some double-counted capacities). The operating capacity of primary aluminum in China was approximately 43.9 million mt. Due to the commissioning of capacity replacement projects, the industry's operating rate increased slightly MoM. In addition, a small batch of technologically transformed capacity in Chongqing resumed production earlier.

Production Forecast: Entering August 2025, the operating capacity of primary aluminum in China will remain at highs. The second batch of replacement projects in Yunnan will be commissioned and achieve production, leading to a rebound in the industry's operating rate. Regarding the proportion of liquid aluminum, currently only a few enterprises have indicated that they will continue to increase casting ingot volumes in August. This is mainly due to weak end-use demand, lower processing fees for alloyed products, and enterprises' pessimistic expectations for August demand, leading to expectations of continued production cuts. This will force aluminum smelters to produce more casting ingots. It is expected that the proportion of liquid aluminum will continue to run at low levels, with limited downside room. Subsequent attention should still be paid to changes in end-use demand and the trend of the proportion of liquid aluminum in primary aluminum.

[Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market exchanges, and SMM's internal database models. These data are for reference only and do not constitute decision-making advice.]